Make Tax Administration Sexy Again!

An expanded version of my notes for a panel talk at the Canadian Economics Association on Saturday, May 31.

Alright, maybe tax administration has never been sexy and MTASA doesn’t exactly roll off the tongue, but hear me out! If you care about tax policy, if you care about public policy, if you care about good government, you should spare a thought for the overlooked area of tax administration.

In an upcoming issue of the Canadian Tax Foundation’s publication Perspectives on Tax Law and Policy, I argue that Canada needs to bring (or drag) its tax administration systems into the 21st century as part of the emerging consensus to “build baby build” to give ourselves insurance against further risk from geopolitical (ok American) upheaval. I also talked about tax administration at a panel at the CEAs over the weekend. Here’s an expanded version of what I said (because I appreciate good moderators who keep speakers to time):

The tax system has lots of jobs

It’s hopefully not a controversial statement to say that good tax policy efficiently and neutrally raises revenues for government. Ie, we want the costs of raising the revenue to be low, and we don’t want the tax to distort economic behavior — well, except when we do, like when we want firms to feel the incentive effects of credits for R&D or consumers to reduce their consumption of bad things (like booze and smokes). So we need to think about the administration of taxation both as part of the cost of the system and also because we don’t get the hoped-for behavioral effects if people or firms face so much administrative burden that they opt out of the tax incentives on offer.

Plus, we get our tax system to do a lot of other jobs beyond raising revenues. It’s our program integrity wizard, checking to see who’s eligible for income-tested programs and collecting repayments on things like EI or student loans. If you care about fellow Canadians getting programs they are eligible for, or if you care about fellow Canadians NOT getting programs they AREN’T eligible for, you should care about tax administration.

Finally, the income tax system is also the main way we, as a country, collect data on household incomes for research and policy-making. Want to know how many kids in Canada are in poverty? You get data from the T-1 personal income tax return. Want Census data on income? Yeah, those are from the T-1 return. Canadian Income Survey? T-1. Survey of Financial Security income variables? T-1. I’ll stop. You get the point. If you want evidence-based policy-making and research to happen in this country, you should care about tax administration.

Administration of returns

As a background paper (by Shaw, Slemrod and Whiting) for the Mirlees Review in the U.K. noted, tax collection systems generally fall into either A) systems where the tax agency takes care of reconciling what the taxpayer has paid against what the taxpayer owes in taxes for the tax period (generally the tax year), or B) systems where individuals have to do their own assessment and reconcile what they owe against what they’ve paid.

You know the drill, if you paid more than you owe, you get money back, otherwise you make a payment to bring your account into balance. That happens in either system A or B. The difference is on whom the onus (and cost) falls to do the work of the calculation. In both systems, taxpayers can dispute what the tax agency claims and the tax agency can dispute what the taxpayer claims. There are procedures for administrative and, if necessary, judicial review. And no, neither system perfectly captures ALL taxpayers. For example, the U.K. has a tax-agency reconciliation system but self-employed persons, business owners, and people claiming capital gains income all have to submit a self-assessed return. But roughly 3 in 5 taxpayers in the U.K. do NOT have to submit an annual tax return.

Here in Canada, we rely on voluntary self-assessment. Yep. That’s right. It’s voluntary. Generally, Canadians are NOT legally required to complete an annual tax return. An overwhelming majority of us do, maybe because we want a refund, or because we know that money we depend on (like child benefits and seniors’ benefits) stops being paid if we don’t, or maybe because it feels patriotic and ethical to fund the costs of democracy. But some non-trivial share of Canadians in a given year do NOT file a return (Saul Schwartz and I estimated it was 12% of working age Canadians; the CRA says it’s 8% of the general population and higher among vulnerable groups). When people don’t file:

we miss out on their data for research and policy,

they miss out on programs they might otherwise be entitled to, and

we miss out on the full effectiveness of welfare enhancing public programs administered using tax return information.

We do have some estimates of the costs in Canada for each system. Vaillancourt and Li (2024) have looked at our current voluntary self-assessment system and estimated that individual returns cost an average of $130 — reflecting both direct out-of-pocket costs (like software or professional fees) plus time spent on the task. Staff working for the Parliamentary Budget Officer have estimated that having the tax agency automatically assess some returns would come with administrative costs of $19 per return. Look, whatever your priors, $19 vs $130 per return sure sounds like it’s administratively more efficient.

What if, instead of the status quo, we tried to increase automation where we can?

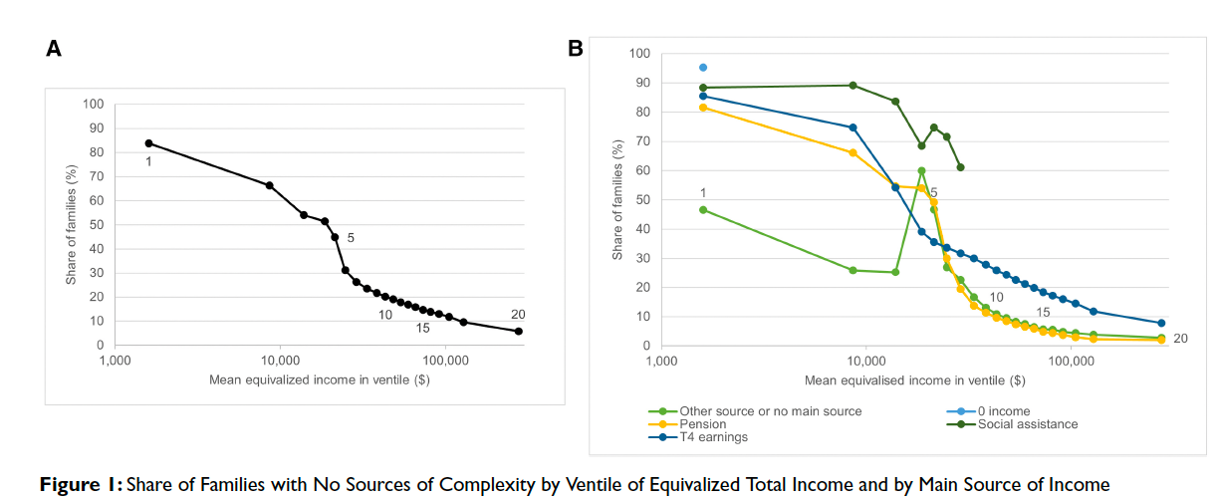

Ok, we’re not gonna’ flip from self-assessment to full-on tax-agency reconciliation overnight and maybe we shouldn’t. But there’s room for efficiency gains. In a paper with Antoine Genest-Grégoire and other colleagues, we’ve estimated that a lot of lower and modest income people, especially those who rely on social assistance income, have returns that probably wouldn't be very hard for the Canada Revenue Agency (CRA) to reconcile taxes paid against taxes owed.

So, what if Canada opted for a hybrid between systems A (tax agency reconciliation) and B (voluntary returns) to did more automation of returns where possible? It might lower the marginal compliance costs, increase the value of T-1 return data, and improve the effectiveness of public incentive programs by making sure that eligible people could actually qualify.

Administration of payroll

Those of us who pay our income and payroll taxes through deductions at source can forget that a big and really important part of what the CRA does is collecting and recording payroll remittances. Different employers file using different methods (including phone, online or even on paper). When employers use software to work out their payroll, they still have to export their information and input it into CRA’s system. Different employers also file payroll remittances according to different schedules that range from once a week to four times a year. Those schedules are set by the CRA, not according to the natural pay-cycles of those businesses.

According to materials published by the CRA, the National Payroll Institute has estimated that the current system of payroll administration costs employers $12.5B annually.

The way we run payroll reporting in Canada also means we’re missing out on useful data for research and policy making. Right now, the payroll administrative data is fed into the Survey of Employment, Payrolls and Hours (SEPH), a monthly survey of 15,000 employers that is combined with a census of the payroll data sent in to the CRA during a one week sample. The survey is released 2 months after collection, so it’s always backwards-looking. It can only report on gross counts of employees (since that’s all that employers report), and struggles with the kind of local data that can matter when, say for example, you’re in a volatile and ridiculous trade war that is hitting different communities very differently.

What if, instead of the status quo, we started to build a better system?

Other countries like the United Kingdom, Ireland and Australia instead use real-time payroll reporting or epayroll. It can let employers report on cycles that reflect their actual paydates. It can let employers directly upload data seamlessly from their existing payroll software tool, or using a software tool paid for by government. Policy-makers would get real-time data to monitor changes in payroll levels. Departments that run programs like EI might be able to let go of the need for the Record of Employment or even weekly earnings reports for people on benefits, because they would have access to better administrative data. At the provincial level, it would be easier to verify who has returned to work after a workers’ compensation claim or to verify self-reported wages for people on social assistance. It would probably also be easier to identify employers that are misclassifying workers as “independent contractors” instead of employees. These would be useful things for federal and provincial governments and the taxpayers that fund them.

Look, building out a new system would be a lift. Some parts of the federal government have been studying this for more than a decade. There are reasons this hasn’t already been done.

In 2021, there was a federal budget commitment to have the CRA design a system. I was part of one external advisory group on that, but then the work just went away… The epayroll work is mentioned in the 2021 transition briefing materials for the federal Minister of Revenue, but it’s nowhere in the 2023 or 2024 transition materials that were released to the public by the CRA. The April 2025 materials for Minister Champagne, who is both Finance and CRA minister, also didn’t mention the project.

If you follow the news, very, very carefully, you can spot public reports of tariff-related lay-offs at employers like Ivaco Rolling Mills, Stellantis and affiliated parts producers, General Motors, and the Canada Metal Processing Group. But generally, these layoffs won’t show up in national or even regional employment data. If employers were to take up the wage subsidy program in the EI system (under the Job-Sharing Agreement), they would still have to do detailed reporting on which employees were paid what wages, on top of their usual payroll reporting.

Why the federal government isn’t already looking to have the CRA test an epayroll system in a pilot project is totally beyond me. They would get real-time data, cut the administrative burden on employers and workers, and get a better input for running public programs. The universe will just keep sending us the same lesson to learn until we finally do.

Administration and governance of the tax agency

Why epayroll just fell off the transition brief of priorities at the CRA despite a public commitment in a budget by the same government, and why the CRA isn’t already being asked to test a pilot epayroll system, are both interesting questions to ponder.

There are other parts of the transition binders for new CRA ministers that offer some clues. New Revenue Ministers are reminded that they can “discuss broad policy issues and direction, and […] help guide our activities” at the CRA. But Ministers of Revenue don’t have the “management and direction” of the agency that is commonly seen in the administrative legislation for most other federal ministers with departments that support them.

Instead, the CRA is set up as a national and not a purely federal part of the machinery of government. It has a Board of Management with members that are nominated by provinces (as well as federally-nominated members and one for the Yukon). It’s the Board, not the Minister, that oversees the management and operations of the tax agency. On the one hand, we REALLY don’t want a tax agency whose operations are politicized. None of us wants a scenario where the Minister of National Revenue is picking which charities to audit or which individual businesses can get valuable tax credits. And, in a decentralized federation where provinces have their own, independent right to levy taxes, provinces should have a say in the operations of the agency that is collecting their taxes, not just federal ones. But if the Parliament of Canada, that represents ALL Canadians, has voted in favour of policy direction and spending for the CRA to get something done, that should matter too,

So, maybe it’s time to open up the administrative legislation that created the CRA. If we want to build tax collection and payroll administrative systems that are in the national interest, dare I say even projects of national interest, then maybe those should be made explicit in the legislative mandate of the Minister of Revenue and, by default, the Agency to whom that mandate is delegated.

Look, if I haven’t convinced you that tax administration can be sexy policy stuffy, I hope more of us might pay attention to the fact that it matters and we could be doing so much better.